How COVID-19 Helped Revive a Fumbling Alternate Mobility Market

How COVID-19 Helped Revive a Fumbling Alternate Mobility Market

Mobility startups have profited from bullish investor sentiment, the presence of 'easy capital' via SPACs, and a post-pandemic push towards sustainable transport networks

A hearty welcome to the 20th edition of The Logistics Rundown, a weekly digest that aims to put some perspective on what’s brewing within the logistics industry. This is a space where we religiously dissect market trends, chat with industry thought leaders, highlight supply chain innovation, celebrate startups, and share news nuggets.

While it is evident that COVID-19 has brought chaos and uncertainty into supply chains, the same is not true of the emerging mobility tech segment. The mobility segment pre-pandemic was faltering on its tracks, as incumbent players realized the issues with running a business that had remarkably low economies of scale, eventually squeezing the investment flowing into the market.

But to elaborate on why that happened and how COVID-19 helped revive the industry, we go back in time to the rise and fall of the Chinese bike-sharing market. By the mid-2010s, bike-sharing companies grew exponentially across China, quickly becoming the flagbearers of sustainable urban transport. While there's no new technology to boast off in this market, the business revolved around the idea of popularizing 'shared ownership' against the usual setup of owning your means of mobility.

What followed was a lesson for urban planners and micromobility-backing venture capitalists on how botched attempts at introducing change could result in far wider repercussions. Initially, several Chinese bike-sharing startups saw meteoric success with raising VC money, helping them flush city streets with thousands of bikes. With users allowed to pick up bikes from anywhere and drop them anywhere within the city without issue, the city nerve centers—like railway stations and parking lots—started overflowing with bikes.

This led to the next problem. As users had zero liability on the assets, bikes inevitably fell prey to rough handling and vandalism. City administrations across China promptly realized a growing problem—their streets and parking spaces were not built to handle such a large influx of bikes on such short notice. What resulted was a meltdown, as bike-sharing business valuations crumbled as quickly as they went up, leaving tens of thousands of unusable and unwanted bikes littered across city streets.

What resulted was a meltdown, as bike-sharing business valuations crumbled as quickly as they went up, leaving tens of thousands of unusable and unwanted bikes littered across city streets.

So, what exactly was the problem? It surely wasn't demand—people continue to be interested in sustainable means of transport. Ironically, the issue was with excessive supply and with how companies, in their rush to raise investment and expand, forgot their unit economics and looked solely at growth—even as they continued burning through billions of dollars in operations.

While something similar nearly played out in the US, city officials did learn a few lessons from the Chinese debacle and enforced laws before the situation got worse. This included regulations on where to park, the number of bikes that could be deployed, and where they could be ridden. Cities also have a cap on the number of micromobility players in the said market, helping them tightly control the bike inflow.

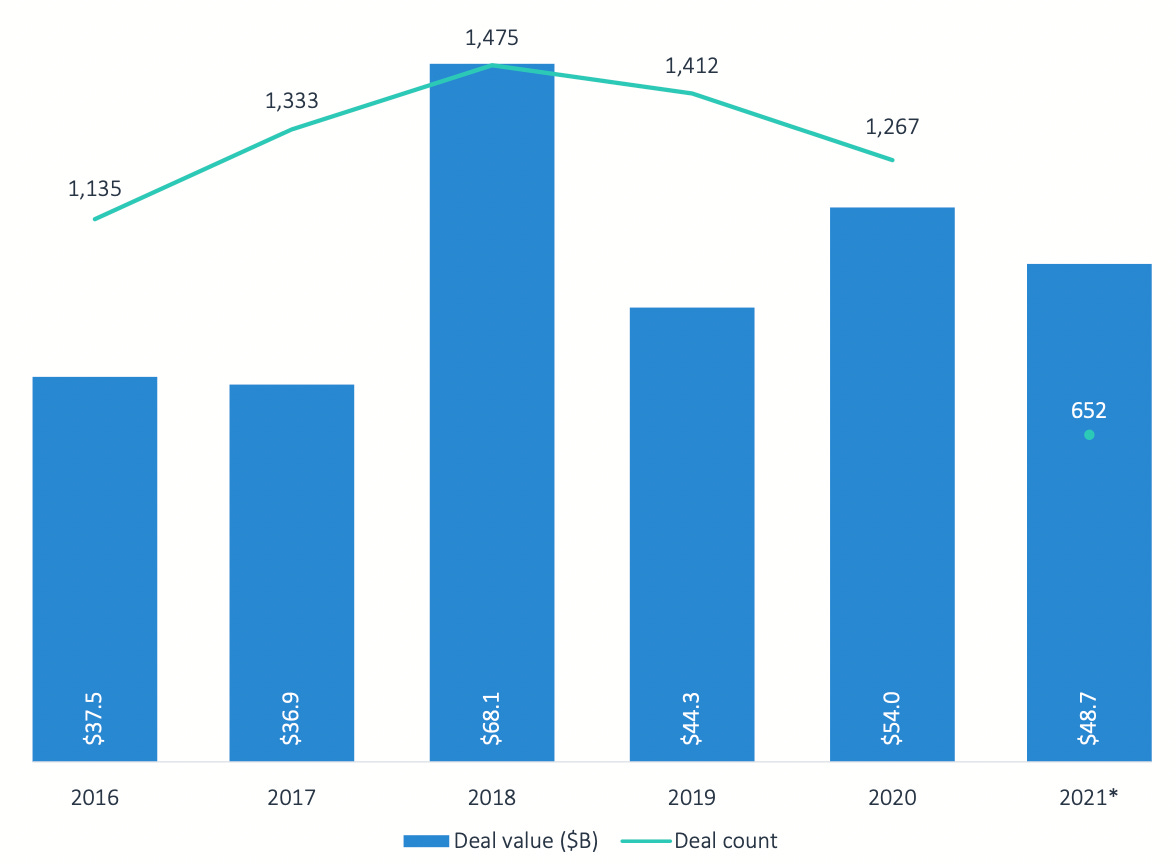

Fast forward to 2021, and the mobility segment—not just micromobility—is seeing a revival. How do we know this? By following the trail of venture capital investment finding its way into the segment. TLR spoke with Asad Hussain, senior analyst of emerging technology at market data platform PitchBook, to understand how the industry is faring of late.

To begin with, while capital investment in the mobility tech segment has not reached its 2018 levels over the last two years, 2021 is likely to cross that figure. VC investment activity in mobility technology this year has already crossed 2019 figures and continues to remain strong.

VC investment activity in mobility technology this year has already crossed 2019 figures and continues to remain strong.

"After the boom-bust cycle of micromobility, there was increased skepticism among investors towards mobility, as they started to regard it more as a low-margin, highly capital-intensive industry. However, since COVID-19 happened, investors and communities have realized how fundamentally broken our transportation systems actually are, and thus there's a lot of enthusiasm back into it for improving transport systems across different lines—like accessibility, convenience, affordability, and sustainability," said Hussain.

Investment has also picked up after mobility companies found a new way to drive money into the market—SPAC exits. A SPAC is a special purpose acquisition company with no commercial operations. It solely exists to raise capital through an initial public offering (IPO) to acquire an existing company, which in this case, is the mobility startup. With stock markets on a tear, several companies went the SPAC route over the last year, raising millions and investing them back into their business.

Easy access to capital has again pushed companies to prioritize growth and expansion over profitability. Grab, one of the biggest mobility companies globally, went public at a $40 billion valuation in 2020—25 times its 2020 sales. However, the company is not expected to break even until at least 2022. And even that is a big 'if.'

Hussain explained that while concerns on profitability are still in the picture, companies and investors believe that profitability lies in building sustainable mobility services in high-income, densely populated cities. "The mobility model is going to move more towards fleet-owned, especially as transport systems transition to electrification and operating costs of vehicles decline."

While concerns on profitability are still in the picture, companies and investors believe that profitability lies in building sustainable mobility services in high-income, densely populated cities.

Vertical integration is also critical to profitability. Hussain spoke of Revel, a Brooklyn-based mobility startup building out its fleets of e-mopeds and bikes while also developing its own charging hubs and employing its drivers—rather than depending on gig economy workers. Vertical integration could improve system efficiencies while also giving their workforce a stable income.

"I think that will be the focus moving forward. What are these workers actually being paid? Are you accounting for the maintenance depreciation and fuel costs these workers pay for today? What does sustainability look like from a labor perspective? I think these are factors that are going to continue heightening in importance," said Hussain.

That said, for alternate mobility systems to pick up, the government needs to play a more prominent role. Cities need to invest in their future, specifically to hit their decarbonization goals. Limiting congestion on city roads can only be done if people get out of their cars and start sharing or renting out mobility assets. Hussain contended that the future would see a mix of personally-owned vehicles, subscription-based vehicle renting, and shared mobility services.

"While the industry has seen an explosion in valuation growth of publicly-traded mobility companies, this has not impacted the really early-stage mobility startups in the same way," said Hussain. "There's definitely an increase in investment in that segment, but not in tandem with the public markets. However, there's enthusiasm amongst investors in the space, and I believe startups will take advantage of it. We are at the early innings of a decade-long transformation in our transport systems, and that's exciting."

The Weekly Roundup

🚢 With freight capacity availability being a severe issue, it is no surprise that empty containers are in massive demand. The Shanghai International Port Group (SIPG) has set up a center to ensure empty containers move out from the Shanghai port without hiccups. SIPG has created a container dispatching center, stored as part of a 450,000 sq. meter empty container transfer yard.

🚚 The US trucking market has been on a perennial increase, even as capacity availability remains strained. With the holiday shopping season fast approaching, it is likely that the prices would not fall back to 'normal levels' anytime before 2022. The Bureau of Labor Statistics data shows that long-haul truckload pricing rose by 23% from June last year to June '21.

📦 While e-commerce sales have gone through the roof, its associated last-mile segment is feeling a crunch with finding enough drivers to deliver the packages. In August, courier jobs climbed by 8,100 jobs month over month, but reports suggest that the rise is not proportionally enough to justify the demand. In a report by Scandit, 37.8% of last-mile delivery firms said finding qualified drivers remains their biggest issue.

⚓ COVID-19 has resulted in the closure of yet another Chinese port at Ningbo-Zhoushan, which ranks among the world's busiest. The shockwaves from this closure will run deep, certainly impacting the West Coast ports of Long Beach and Los Angeles. With the holiday shopping season on the horizon, such a development is a cause for concern. This has also increased fears of a larger breakout across other neighboring ports, which could result in a large-scale logistics disaster.

...said who?

"Our strategy has been to provide a more integrated solution. So we are moving from shipping containers from port to port to shipping from door to door. For that to happen, we need to grow our capabilities on shore. Now, we are looking to be able to deliver goods from Asia to the U.S., not just to the port but also to someone's door."

- Maersk CEO Soren Skou commenting on how the container line is improving its reach through vertical logistics integration

Want to talk with us? Have something you'd like us to cover? Drop your thoughts to vishnu@truckx.com

We are TruckX, the Internet of Things plug to logistics. Check us out at www.TruckX.com