Running Circles Around Volatile Consumer Demand And Inflammated Freight Networks

Running Circles Around Volatile Consumer Demand And Inflammated Freight Networks

Shippers are battling transport bottlenecks, procurement uncertainties, chaotic consumer demand, and high operational costs as they make their way to the peak season

A hearty welcome to the 49th edition of The Logistics Rundown, a weekly digest that aims to put some perspective on what’s brewing within the logistics industry. This is a space where we religiously dissect market trends, chat with industry thought leaders, highlight supply chain innovation, celebrate startups, and share news nuggets.

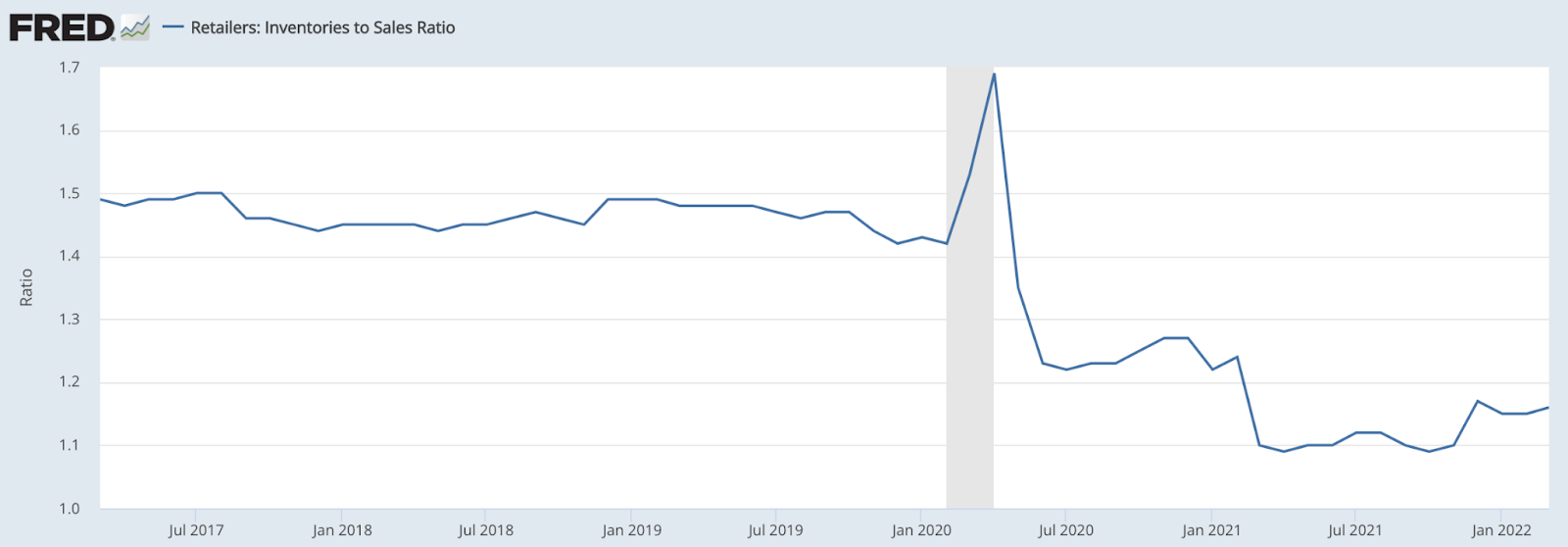

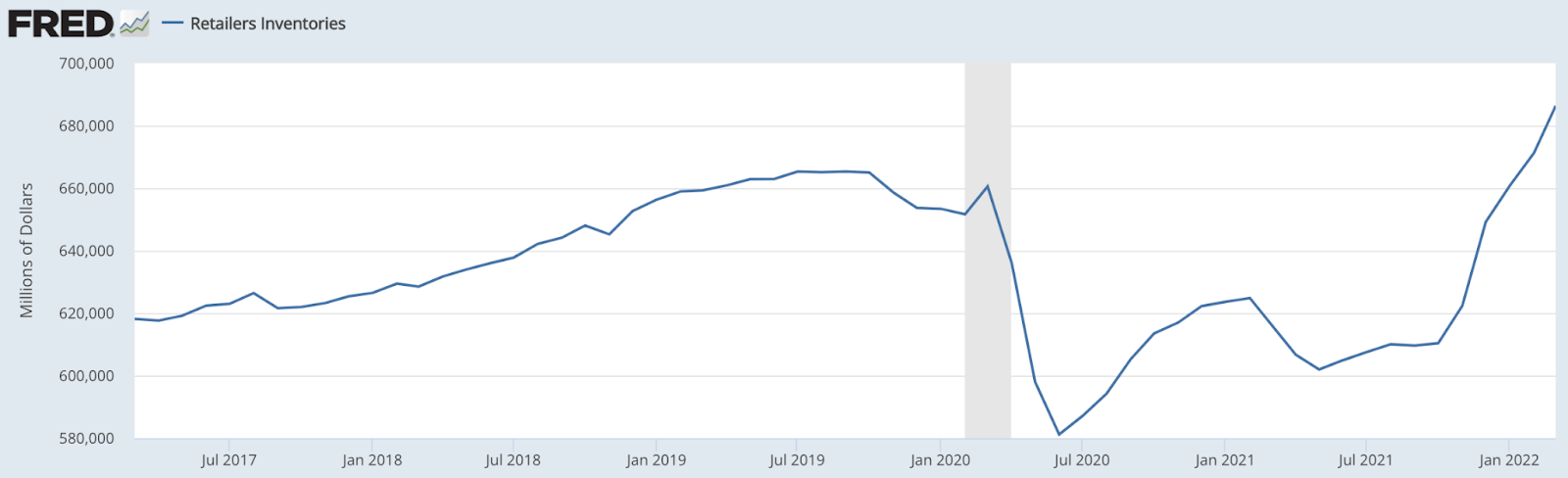

There are several economic indicators out there helping reflect the true extent of the rise in consumer demand at the onset of the pandemic, like consumer spending and retail sales. But to understand the difficulty shippers had in managing this particular market volatility, it makes sense to compare the retail inventories to sales ratio and the available inventory storage space in the country.

After an initial spike, the FRED inventories to sales ratio continued to cascade much through the COVID-19 season, falling from a pre-pandemic average of over 1.4 in Feb ‘20 to less than 1.1 by Dec ‘21. In parallel, the increase in real inventories across the US shows that inventories are not falling per se, but rather, sales outstripping retailers’ ability to stock inventories on time.

The Logistics Managers’ Index (LMI) measures the pain of shippers quite clearly. While it is understood that dry van trucking volumes are tipping, the inventory levels stacked up in warehouses are some of the highest on record, with LMI documenting 72.3 on its diffusion index (a reading over 50 would mean positive growth to the metric). Although down from the historic high in Feb ‘22, it’s still the third-highest recording ever.

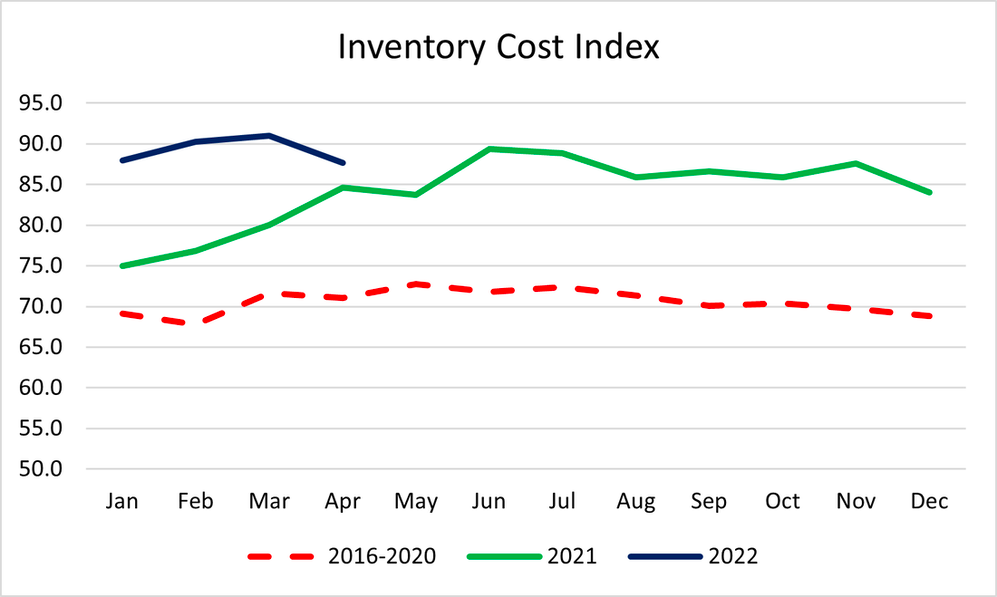

Aside from inventory space drying up for shippers, the costs of holding inventories are also stifling operations. LMI’s inventory costs index has been plateauing for about a year, but at extremely high levels. The Apr ‘22 recording of 87.7 is stunningly high, considering a reading of 100 would theoretically be the most pain a shipper can feel in terms of costs.

With this being the warehousing story, the much-advertised transport bottlenecks have piled on the misery, as shippers scrambled for freight capacity at double or triple pre-pandemic rates. The peak delays at the US West Coast came at an inopportune moment, across the later half of ‘21, when shippers were readying inventories for the holiday shopping season.

The delays meant that many inventories that were bought to be sold during the shopping season ended up reaching the US shores after the season was over. All these metrics, indices, and macroeconomic factors culminate in the picture of shippers who are clearly lost with their forecasts on what is stocked, when it is stocked, where it will be stocked, and for how long it will be stocked. Clearly, it is hard to do business in such an environment.

All these metrics, indices, and macroeconomic factors culminate in the picture of shippers who are clearly lost with their forecasts on what is stocked, when it is stocked, where it will be stocked, and for how long it will be stocked.

The meteoric rise of e-commerce to fill the gaps ceded by physical retail during the quarantining period is another headache to shippers. Consumers have learned to expect stuff delivered to their houses on a flexible schedule and in quick time. Products moving via direct-to-consumer channels pose a challenge as shipping goods individually would cost more and take more space on a truck than consolidated cargo that moves on pallets.

E-commerce has led to a situation where shippers are expected to stock more than they usually would, considering demand needs to be fulfilled at breakneck speed. Factors like these inevitably impact shipper bottom lines, and considering retail is a low-margin, high-risk business, stakeholders need to rethink strategies to tighten operations.

“A lot of retailers have understood the need to build core warehousing infrastructure that has a spread out footprint. By having local warehouses across regions, shippers maintain flexibility, rather than shipping everything from the home territory,” said Fran Quilty, the CEO and co-founder of Conjura, an e-commerce data analytics platform. “When businesses are scaling, they try becoming more systematic. If you’re a British business, having a warehouse in Europe, the US, and Asia will help you set up a good customer service protocol.”

Data helps a lot with deciding the specifics behind inventory stocking. Consider a business selling both on Amazon and on its own site. Operations get a bit complex as the company will likely have some territories serviced only through Amazon and a few areas where it can take care of fulfillment in-house.

“If you’re looking for repeat orders from customers, you’d need to understand the platform their orders were fulfilled on, the return rates in the region, the cost of delivery, optimizing delivery times, and the likes. Businesses focused on such metrics will learn to identify issues before the flare, and that can be a competitive advantage,” said Quilty.

Quilty explained how tools surrounding marketing and customer analytics were not cloud-based and were more fragmented for a long time, but now things are looking up due to greater integration possibilities with API. “At Conjura, we get access to data quite easily, rather than tussle with gnarly integrations into warehouse management systems. This translates to more information for operators, helping them manage the business better,” he said.

Better visibility into operations has enabled shippers to monitor their service providers better, and make the calls when deliveries weren’t meeting service level agreements (SLAs). Improved access to data leads to tighter management, which leads to better service.

Companies competing against retail behemoths like Walmart and Amazon can work with third-party aggregation businesses like co-ops that roll up volumes to get better freight rates. “Such aggregators can just go after Shopify e-commerce stores of a certain size, roll them up for a better buying power. This is happening in several different segments, and I think it will only get bigger,” contended Quilty.

Companies competing against retail behemoths like Walmart and Amazon can work with third-party aggregation businesses like co-ops that roll up volumes to get better freight rates.

But at the end of the day, the core infrastructure and transport strategies of companies are heavily dependent on the retail vertical they fall under. “We work alongside pet retailers with a very stable, high repeat order business, and deal with fashion retail where the business is more volatile and dependent on trends. Every company approaches its logistics differently,” said Quilty.

To understand when the tide is changing, it pays to look at the engagement score of customers to understand buyer sentiment. Quilty mentioned that when customers are not opening emails that frequently or not interacting on social media or on the site, it could be a moment to ponder. “Often, interaction is the first metric to fall before purchases actually see a drop,” said Qulity. “Observing little data points like this can really help improve both the top line and bottom line for operators. Today, we see a good change in the market — the operational side of the business is really embracing data more than ever before.”

The Weekly Roundup

There is trouble in the state of California, as its power grids are being battered by the rise (and use) of electric vehicle charging stations. California’s push towards electrification is well known, with the state looking to transition to a non-fossil reality by 2045. But there are critical gaps in this roadmap, as aside from the logistics and transport segment, the power grids need a major revamp.

FMCG major Nestle is airlifting infant formula to the US as it reels from a baby food crisis that is leaving supermarkets empty. Aside from picking up shipments from the Netherlands and Switzerland, Nestle is also boosting production to alleviate the crisis. The US FDA has made imports more flexible for alternative formulas, with Nestle reporting that it is assessing the guidance provided to ensure faster customs clearance.

While used truck prices have come down over the last couple of months due to cooling truckload capacity demand, they still are valued at rates much higher than pre-pandemic. JD Power, which releases a monthly report on prices of new and used Class 8 tractors, mentioned that 4- to 6-year-old sleeper cabs have depreciated 6.9% every month on average since the start of ‘22.

Ocean liners are watching the fall in maritime spot rates across the transpacific and transatlantic trade lanes and increasing their blank sails to ensure balance. This tightening of capacity has led Asia-US West Coast spot rates spiking over 15% to roughly $14,000 per FEU, and the Asia-US East Coast settling down at prices around $16,000 per FEU. Meanwhile, regulators are on the sidelines, observing liner behavior for evidence of unfair practices.

…said who?

“There are many measures we have had to put in place, but this one, this undoubtedly has had a resounding effect.”

- Gene Seroka, the Port of Los Angeles executive director, while commenting on the effectiveness of the penalty threat to leaving containers at the port terminal, pushing shippers to retrieve their containers quicker

Want to talk with us? Have something you'd like us to cover? Drop your thoughts to vishnu@truckx.com

We are TruckX, the Internet of Things plug to logistics. Check us out at www.TruckX.com